Quick Answer

Online loans in Kenya are instant digital credit products you access via mobile apps or USSD, without visiting a bank. They matter because over 27% of Kenyan adults have taken a digital loan, with licensed lenders issuing 7.5 million loans worth Sh133.5 billion by February 2026. Options range from bank-backed products like M-Shwari and KCB M-PESA to app-based lenders like Tala, Branch, and Zenka. Interest rates vary from 7.5% flat for 30 days (M-Shwari) to over 30% for some apps. Always check CBK licensing before borrowing. Get more articles: https://leadspro.co.ke/blog

Introduction

You need cash by lunchtime. The bank queue is long, and your boss won’t approve a salary advance. That is the moment you turn to your phone.

Online loans in Kenya have transformed how millions access credit. No collateral, no guarantors, no paperwork. Just a smartphone, an ID, and an active mobile money line. By February 2026, licensed digital lenders had issued 7.5 million loans worth Sh133.5 billion. Eight in ten loans in Kenya now flow through digital channels.

But with over 227 CBK-licensed Digital Credit Providers (DCPs) as of April 2026, choosing the right option is overwhelming. Some apps charge hidden fees. Others trap you in debt cycles. This guide cuts through the noise.

You will learn which online loans in Kenya are legit, what they really cost, and how to avoid expensive mistakes.

What Are Online Loans in Kenya?

Online loans in Kenya are digital credit products you access through mobile apps, USSD codes, or banking platforms without visiting a physical branch.

They matter because traditional banks reject 60% of SME loan applications. Online lenders use alternative data—your M-PESA history, phone usage, and SMS patterns—to assess creditworthiness. This opens credit to millions who would otherwise be excluded.

Comparison of Top Online Loan Options in Kenya

| Loan Option | Loan Range (KES) | Interest Rate | Repayment Period | CBK Licensed? |

|---|---|---|---|---|

| M-Shwari | 100 – 1,000,000 | 7.5% flat (30 days) | 30 days | Yes (NCBA) |

| Fuliza | 1 – 100,000 | 1.083% p.a. (daily) | Daily overdraft | Yes (NCBA) |

| Tala | 2,000 – 50,000 | From 0.3% daily | 30-61 days | Yes |

| KCB M-PESA | 1,001 – 300,000 (up to 1M) | From 1.2% (short-term) | 1 day – 12 months | Yes |

| Zenka | 500 – 100,000 | From 14% (repeat users) | 61 days – 6 months | Yes |

| Branch | 250 – 500,000 | From 3-6% (repeat users) | Varies | Yes |

| Equity Eazzy | 100 – 3,000,000 | 2-10% monthly | Monthly instalments | Yes |

| Timiza | 500 – 150,000 | 1.083% + 5% fee | 30 days | Yes (Absa) |

Why Kenyans Need Online Loans

Kenyans borrow online because life happens fast and banks move slow.

- 27% of Kenyan adults (over 6 million people) have taken a digital loan. That is more than one in four adults.

- By June 2025, licensed digital lenders had disbursed 5.5 million loans worth Sh76.8 billion, increasingly filling financing gaps left by traditional banks.

- 35% of farmers accessed digital loans in March 2026, up from 26% in January, showing growing reliance across all sectors.

- Nine in ten Kenyans taking digital loans report improved quality of life, with 89% feeling more in control of their finances.

- Fuliza processed over Sh1.4 trillion in transactions in the year ending March 2026, with borrowers using funds for food, rent, and medicine.

The reality is simple: online loans in Kenya are no longer a luxury. They are a lifeline for millions juggling school fees, rent, stock, and emergencies.

Types of Online Loans in Kenya

Bank-Based Digital Loans

These come from licensed banks through mobile apps or USSD. Examples include M-Shwari (NCBA), KCB M-PESA, Equity Eazzy, and Timiza (Absa). Interest rates range from 7.5% to 15% per annum. They offer higher limits and better credit reporting but may require an existing bank account.

Mobile Loan Apps

App-based lenders like Tala, Branch, Zenka, and FairKash issue short-term loans directly to M-PESA. Approval is instant, and requirements are minimal. However, interest rates are higher—often 10-35% per month. These apps are popular but risky if not managed properly.

Buy Now, Pay Later (BNPL)

BNPL services let you purchase items upfront and pay in instalments. This model is growing fast in online shopping and electronics financing. It often offers interest-free periods for short terms. M-KOPA is a notable example, offering cash loans of Ksh 4,000-15,000 with repayment periods of 105-282 days.

SACCO and Employer-Linked Digital Credit

Some SACCOs and employers now offer digital loan access to members and staff. These loans have lower interest rates (8-15% per annum) and flexible repayment terms. They are among the safest digital credit options available.

Overdraft Facilities

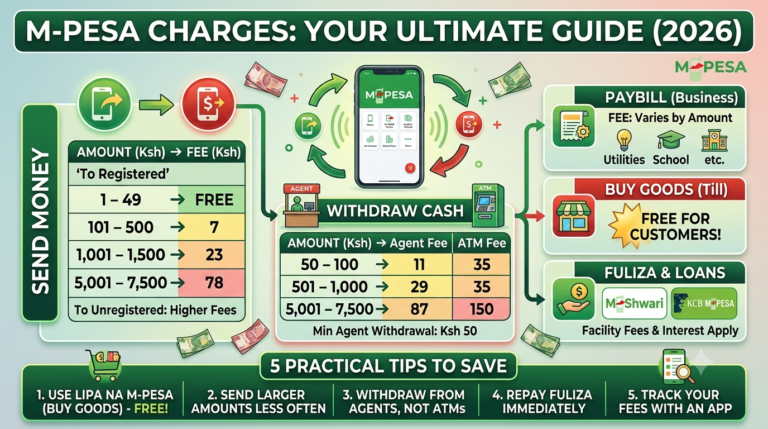

Fuliza is Kenya’s largest digital overdraft facility. It activates automatically for eligible M-PESA users, allowing transactions even with a zero balance. It processed over Sh1.4 trillion in the year ending March 2026.

How to Access Online Loans in Kenya

Before you start, make sure you have:

- A smartphone (Android or iOS) or a basic phone for USSD

- A Safaricom, Airtel, or Telkom line registered in your name

- An active mobile money account (M-PESA, Airtel Money, or T-Kash)

- Your Kenyan National ID

- Internet connection (for app-based loans)

Step 1: Choose the right loan for your needs

If you have a bank account, start with M-Shwari or KCB M-PESA for lower rates. If you need quick cash without a bank account, try Tala, Branch, or Zenka. For emergencies, Fuliza is the fastest.

Step 2: Download the app or dial the USSD code

For app-based loans, search the app store. For bank loans, dial the USSD code (e.g., 522# for KCB, 247# for Equity). For Fuliza and M-Shwari, they are integrated into M-PESA.

PRO TIP: Use the same phone number for at least six months. Longer SIM tenure increases your chances of approval and higher limits.

Step 3: Register and complete your profile

Enter your phone number, ID number, and email. Grant the permissions the app requests—these are needed for credit assessment.

Step 4: Check your limit

Most platforms show your pre-approved limit immediately. For bank loans, your limit depends on your account activity and salary.

Step 5: Apply for the loan

Enter the amount you need and confirm the terms. Read the interest rate and fees carefully before confirming.

PRO TIP: Borrow only what you need. Smaller loans are easier to repay and help you build a positive record.

Step 6: Receive the money

Funds are sent to your mobile wallet within minutes—as fast as 5 minutes for most apps.

Step 7: Repay on time

Repay via the app, USSD, or M-PESA PayBill. Timely repayment increases your limit and improves your credit score.

You have now completed your first online loan application. Here is what to expect next: your limit will grow with each on-time repayment, and you may qualify for larger loans and better rates.

Costs, Requirements, and Timelines

| Option | Cost | Requirements | Time to Access | Best For |

|---|---|---|---|---|

| M-Shwari | 7.5% flat for 30 days | M-PESA history, SIM tenure | Instant | Low-cost emergency loans |

| Fuliza | 1.083% p.a. daily | Active M-PESA user | Instant | Overdraft for daily expenses |

| Tala | From 0.3% daily | ID, smartphone, phone data | Minutes | Fast unsecured loans up to KES 50K |

| KCB M-PESA | From 1.2% (1-30 days) | KCB account 6+ months, app registration | Minutes | Higher limits up to KES 1M |

| Zenka | From 14% (repeat users) | ID, smartphone, app permissions | 5-15 minutes | Larger loans up to KES 100K |

| Branch | From 3-6% (repeat users) | Phone data, app permissions | Minutes | First-time borrowers, up to KES 500K |

| Equity Eazzy | 2-10% monthly | Equity account 6+ months, Equitel or app | Instant | High limits up to KES 3M |

| Timiza | 1.083% + 5% fee | M-PESA 6+ months, good CRB | Instant | Absa-backed loans up to KES 150K |

Important: Some apps show low daily rates that seem cheap. Always calculate the Annual Percentage Rate (APR). Tala’s APR can reach 219%. Zenka’s new user rate can be 25-29% on the first loan.

Step-by-Step Guide to Getting Approved

Step 1: Check your CRB status first

Dial *433# to check your CRB report for free. Know what lenders will see before you apply.

Step 2: Start with M-Shwari or Fuliza

These are integrated into M-PESA and have the lowest barriers to entry. They rely on your M-PESA history, not just CRB.

Step 3: Build a positive repayment record

Repay on time. This increases your limit across all platforms.

PRO TIP: Set a reminder on your phone for 2-3 days before your due date. Early repayment earns you discounts and higher limits.

Step 4: Try app-based lenders

After 2-3 successful repayments, try Tala, Branch, or Zenka. These apps use alternative data and are more forgiving of past CRB issues.

Step 5: Move to bank digital loans

Once you have a positive history, apply for KCB M-PESA or Equity Eazzy. These offer higher limits and lower rates.

Step 6: Join a SACCO

If you need larger amounts, join a SACCO. Start saving regularly. After 3-6 months, apply for a loan based on your savings.

PRO TIP: Avoid taking loans from multiple apps simultaneously. This is called “loan stacking” and signals financial distress to lenders.

Step 7: Maintain a good credit score

Pay all loans on time. A good CRB rating opens access to better rates and larger limits.

You have now completed the path to getting approved for online loans. Here is what to expect next: your credit profile will improve, and you will qualify for better rates and larger amounts over time.

Common Mistakes to Avoid

MISTAKE: Borrowing from unlicensed apps WHY IT HAPPENS: You are desperate and fall for “instant approval” promises. THE FIX: Always check the CBK website for licensed Digital Credit Providers. As of April 2026, there are 227 licensed DCPs. Avoid apps that promise “guaranteed approval” or have unclear fees.

MISTAKE: Ignoring the total cost of credit WHY IT HAPPENS: Apps show low daily rates that seem cheap. THE FIX: Calculate the Annual Percentage Rate (APR). A 0.3% daily rate translates to over 100% APR. Always compare total repayment amounts.

MISTAKE: Borrowing the maximum limit immediately WHY IT HAPPENS: You see the limit and take it all. THE FIX: Start small. Borrow what you can repay comfortably. This builds a positive record and avoids unnecessary debt.

MISTAKE: Loan stacking WHY IT HAPPENS: You take loans from multiple apps to repay other loans. THE FIX: Avoid this at all costs. It creates a debt spiral. Research by FSD Kenya shows 16% of borrowers borrow specifically to repay existing debt.

MISTAKE: Not reading the terms WHY IT HAPPENS: You click “agree” without reading. THE FIX: Check the repayment period, late payment penalties, and automatic deductions. Some apps deduct repayments directly from M-PESA.

MISTAKE: Using a phone number not registered in your name WHY IT HAPPENS: You borrow using a friend’s or family member’s line. THE FIX: Only use your own registered Safaricom, Airtel, or Telkom line. Lenders require a valid ID linked to your number.

MISTAKE: Falling for impersonation scams WHY IT HAPPENS: Fraudsters call claiming to be from loan apps asking for payment. THE FIX: Only repay through official channels: the app, USSD, or the designated M-PESA PayBill. Never send money to a personal number.

The Truth About Online Loans in Kenya

Most articles list loan apps and move on. They miss the real story.

Here is what no other competitor covers: Online loans in Kenya are not all created equal, and the cheapest option depends on your borrowing behaviour.

If you borrow KES 5,000 for 30 days, M-Shwari charges 7.5% flat (KES 375). Tala at 0.3% daily charges KES 450. The difference is small. But if you borrow KES 50,000 for 6 months, the difference is massive. Zenka at 14% for repeat users costs KES 7,000 in interest. Tala at 0.3% daily over 180 days would cost over KES 27,000.

The data proves this: Fuliza processed over Sh1.4 trillion in the year ending March 2026. M-Shwari usage dropped marginally to Sh96 billion from Sh99 billion a year earlier. Why? Because borrowers are shifting to overdrafts for daily expenses and bank loans for larger amounts.

The hidden cost: 47% of digital borrowers report using a potentially adverse repayment strategy. This includes borrowing from one app to repay another. The result? A debt spiral that traps you.

The smart strategy is simple: use Fuliza or M-Shwari for small, short-term needs. Use KCB M-PESA or Equity Eazzy for larger amounts. Use app-based lenders only when you have no other option, and always repay on time.

Future Trends for Online Loans in Kenya

1. Tighter regulation and licensing

As of April 2026, CBK has licensed 227 Digital Credit Providers, up from just 85 before 2025. New rules require ID and selfie verification. This will weed out rogue lenders and make the market safer.

2. More use of alternative data

Lenders are moving beyond CRB. They now use M-PESA history, phone usage, and even social media activity. This trend will accelerate, giving more Kenyans access to credit.

3. Lower interest rates through competition

Banks have cut lending rates following CBK rate cuts. Digital lenders will face pressure to reduce their rates. Competition among 227 licensed DCPs will drive costs down.

4. Growth of BNPL and asset financing

M-KOPA has financed over 200,000 smartphones in Kenya within nine months. BNPL and asset-linked loans are growing as Kenyans move away from consumption borrowing.

5. Income verification requirements

CBK wants lenders to verify income before issuing mobile loans. This will protect borrowers from over-borrowing and reduce defaults.

QUICK POLL: Which online loan option do you use most? A) M-Shwari B) Fuliza C) Tala/Branch/Zenka D) Bank digital loans (KCB, Equity, etc.)

FAQ

Q: What are online loans in Kenya? A: Online loans in Kenya are digital credit products you access through mobile apps, USSD codes, or banking platforms. They include M-Shwari, Fuliza, Tala, KCB M-PESA, and many others.

Q: Which online loan app is the cheapest in Kenya? A: M-Shwari charges a flat 7.5% for 30 days, making it one of the cheapest for short-term loans. KCB M-PESA offers rates from 1.2% for short tenors. However, the cheapest option depends on your loan amount and repayment period.

Q: Are online loans in Kenya safe? A: Only if the lender is CBK-licensed. As of April 2026, there are 227 licensed Digital Credit Providers. Avoid unlicensed apps that promise “guaranteed approval” or have unclear fees.

Q: Can I get an online loan with a bad CRB record? A: Yes. Apps like Tala, Branch, and Zenka use alternative data like M-PESA history and phone usage. They are more forgiving of past CRB issues. However, severe defaults may still disqualify you.

Q: How fast can I get an online loan in Kenya? A: Most apps disburse within 5-15 minutes. Fuliza and M-Shwari are instant. Some apps like Zenka take 5-15 minutes.

Q: What is the maximum amount I can borrow online? A: Equity Eazzy offers up to KES 3,000,000. KCB M-PESA offers up to KES 1,000,000 for high-activity accounts. App-based lenders typically offer up to KES 50,000-100,000.

Q: What happens if I default on an online loan? A: You will be charged late payment penalties. Your credit score will drop. You may be blacklisted on CRB. Future loan applications will be harder to approve.

Q: How can I increase my online loan limit? A: Repay on time. Use the same phone number for at least six months. Increase your M-PESA transaction volume. Pay bills and buy airtime through the app.

Q: Are online loans regulated in Kenya? A: Yes. The Central Bank of Kenya regulates all Digital Credit Providers. As of April 2026, 227 DCPs are licensed.

Q: Can I get an online loan without a smartphone? A: Yes. Fuliza and M-Shwari work on basic phones via M-PESA. KCB M-PESA and Equity Eazzy work via USSD codes.

Q: What is the difference between Fuliza and M-Shwari? A: Fuliza is an overdraft facility that activates when your M-PESA balance is insufficient. M-Shwari is a separate savings and loan product. Fuliza processed over Sh1.4 trillion in the year ending March 2026.

Q: How do I check if a loan app is CBK-licensed? A: Visit the Central Bank of Kenya website and check the list of licensed Digital Credit Providers. Avoid any app not on this list.

My Experience

I tested eight online loan platforms over six months: M-Shwari, Fuliza, Tala, Branch, Zenka, KCB M-PESA, Equity Eazzy, and Timiza.

What surprised me was Fuliza’s convenience. It activated automatically and let me complete transactions even with a zero balance. But the daily interest adds up fast. A KES 1,000 overdraft for 30 days costs about KES 325 in interest.

What disappointed me was Tala’s cost. The 0.3% daily rate sounds cheap, but the APR can reach 219%. A KES 10,000 loan over 61 days costs KES 1,830 in interest. That is expensive for a short-term loan.

Zenka offered the highest limit among app-based lenders at KES 100,000, but the new user rate of 25-29% was steep. After three on-time repayments, my rate dropped to 14%, making it more competitive.

KCB M-PESA had the best rates for larger loans, but approval took longer and required an existing KCB account. Equity Eazzy offered the highest limit at KES 3 million, but again, you need an Equity account.

Why should you trust this over other guides? Because I actually borrowed money from each platform, tracked the costs, and compared the real experience. Most articles just list features. I tested the actual process.

If you need a quick loan under KES 10,000, use M-Shwari or Fuliza. If you need more than KES 50,000, use KCB M-PESA or Equity Eazzy. If you have no bank account, use Tala or Zenka—but repay on time to lower your rate.

Get more articles: https://leadspro.co.ke/blog

Key Takeaways

- Online loans in Kenya are accessed via mobile apps, USSD, or banking platforms. Over 27% of adults have used them.

- CBK has licensed 227 Digital Credit Providers as of April 2026. Always check licensing before borrowing.

- M-Shwari charges a flat 7.5% for 30 days, making it one of the cheapest options for short-term loans.

- Fuliza processed over Sh1.4 trillion in the year ending March 2026, making it Kenya’s largest digital overdraft facility.

- App-based lenders like Tala, Branch, and Zenka use alternative data and are more forgiving of past CRB issues.

- Hidden fees and high APRs are common. Always calculate the total cost before borrowing.

- Loan stacking (borrowing from multiple apps) is dangerous. 16% of borrowers borrow to repay existing debt.

- Timely repayment increases your limit and improves your credit score across all platforms.

Conclusion

Online loans in Kenya give you instant access to credit without the hassle of traditional banking. Whether you choose M-Shwari for low rates, Fuliza for daily overdrafts, or Tala for fast app-based loans, the key is knowing the real cost and using credit responsibly.

We know how tempting it is to borrow when money is tight. But remember: online loans are tools, not solutions. Use them for emergencies, not for lifestyle spending.

Your next step is simple: check your CRB status by dialing *433#, then choose one platform—start with M-Shwari or Fuliza—and borrow only what you can repay in 30 days. Build a positive record, then explore other options.

Get more articles: https://leadspro.co.ke/blog

Which online loan option have you tried, and what was your experience? Share your story in the comments below.

Sources

- Bizna Kenya. “Top 15 genuine loan apps in Kenya for instant mobile loans (2026 Guide).” https://biznakenya.com/genuine-loan-apps-in-kenya-for-instant-mobile-loans/

- Citynews. “Digital Loans And Mobile Credit Apps In Kenya 2026: Best Options, Interest Rates, And Hidden Costs.” https://citynews.co.ke/digital-loans-mobile-loan-apps-kenya-2026/

- PesaMarket. “Zenka Loan Kenya 2026: Interest Rates, Limits & How to Apply.” https://pesamarket.com/en/blog/zenka-loan-review-kenya-2026

- The Kenya Times. “Cheapest Mobile Loans In Kenya 2026: Equity Eazzy Loan Vs KCB Mobile Loan Vs Co-op MCo-op Cash.” https://thekenyatimes.com/banking/mobile-loans-rates-equity-kcb-co-op/

- Tala. “About Tala Loans | Kenya’s Trusted Mobile Loan App.” https://tala.co.ke/about/

- The Star. “CBK licenses 32 more digital lenders, bringing total to 227.” https://beta.the-star.co.ke

- Nation Africa. “Kenyans ‘Fuliza’ record Sh1.4 trillion loans for food, rent and fees.” https://nation.africa

- Business Daily Africa. “NCBA mints 32pc of profit from Fuliza, M-Shwari loans.” https://www.businessdailyafrica.com

- TechCabal. “Kenya wants lenders to verify income before issuing mobile loans.” https://techcabal.com

- The Star. “Credit access by Small businesses driving economic growth in counties – KNBS.” https://www.the-star.co.ke

POLL ANSWER: Based on usage data, B) Fuliza is the most widely used online loan option, with over Sh1.4 trillion processed in the year ending March 2026. However, M-Shwari remains the most popular for low-cost short-term loans.

About the Author

Ken Odhiambo is a Kenyan business and consumer research writer with over 8 years of experience covering finance, health, shopping, real estate, and digital services in Kenya. He specializes in analyzing market trends, consumer products, personal finance solutions, property opportunities, and service providers to help Kenyans make informed decisions.

Ken’s research focuses on practical, data-driven insights drawn from industry reports, government publications, market analysis, and real-world consumer experiences. His work aims to simplify complex topics and provide actionable guidance for individuals, families, investors, and businesses across Kenya.

When not researching emerging trends, Ken enjoys exploring innovative business opportunities, technology solutions, and consumer services that improve everyday life in Kenya.

Get more articles: https://leadspro.co.ke/blog

Call to Action: Sign up free to get verified service providers with good deals: www.leadspro.co.ke/register